The impact of health on savings and income

4 September 2023

Key points

- Half of working-age people with poor health have no savings whatsoever, compared to 35% with good health.

- At almost all levels of income, more people with poor health lack savings than people with good health.

Being in problem debt can harm people’s physical and mental health by causing strain and stress, reducing income available for products and services that promote good health, or increasing health-harming coping behaviours. Poor health can also increase the possibility of problem debt, for example when someone loses their job or has a low income. This can create a cycle of problem debt and poor health.

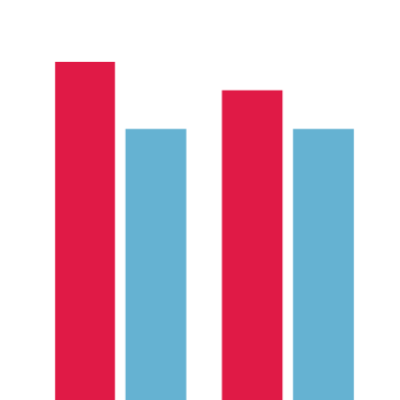

This chart shows the proportion of people with no savings by income and health in 2018-20.

- Overall, half (50%) of people with poor health have no savings compared to just over a third (35%) with good health. This is partly due to people with poor health being more likely to have a lower household income, but not exclusively. At almost every level of income, people with good health are more likely to have at least some savings.

- In the bottom tenth of incomes, 77% of people with poor health have no savings compared to 66% with good health.

- In the top tenth of incomes, 23% of people with poor health have no savings compared to 18% with good health.

- The inequality in savings between people with good health and people with poor health is larger in the bottom tenth of incomes than in the top tenth.

There are several potential explanations for this relationship. One is that people with poor health are more likely to be out of work, and consequently have lower incomes. They may also face higher costs as a result of their poor health, such as higher heating bills or home adaptation costs, leaving them with less remaining income to save.

Working-age people on lower incomes are more likely to have no savings whatsoever. People on low incomes pay extra for essential goods and services because of the poverty premium, which can make it more difficult to accumulate savings. Help to Save is a government scheme for people eligible for Working Tax Credit and Universal Credit. However, the bonuses are not paid until the end of the second year, which may be too long a wait for families experiencing financial difficulties and expensive debt repayments. Instead, a savings scheme should be accompanied by more sustainable and affordable credit.

- The income deciles are based on net equivalised household income (adjusted for household size) after housing costs have been deducted from income. Individuals are grouped into 10 equal-sized bands (deciles). The first decile represents the lowest 10% of incomes and the tenth decile represents the highest 10% of incomes.

- Self-rated health – where people are asked to assess their overall health – is a good proxy for health outcomes generally. Self-rated health has been grouped into ‘good health’: consisting of ‘good’ and ‘very good’ health; and ‘poor health’: consisting of ‘fair’, ‘poor’ and ‘very poor’ health. Respondents are asked how much they have in their savings accounts.